John Van Alst of the National Consumer Law Center has written this comprehensive report entitled Time to Stop Racing Cars: The Role of Race and Ethnicity in Buying and Using a Car.

Here is the executive summary:

For many in America, a car provides not only physical mobility but also economic mobility. Yet for years, studies have shown that the costs of buying, financing, and using a car can vary based on race or ethnicity. A consumer’s race or ethnicity can impact:

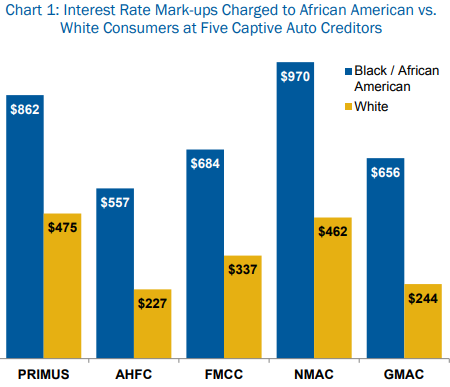

How much it costs to finance a car;

How much a consumer is charged for the car itself;

How much a consumer is charged for add-on products sold with the car;

The ability of consumers to successfully negotiate for better terms;

The rates paid to insure a car; and

The likelihood that civil fines or penalties will lead to suspensions of a driver’s license.

These disparities make cars more expensive for some races and ethnic groups and keep some families from getting a car at all. They contribute to the differences we see in the ability of families to get a car. For those at or below the poverty line, 13% of White households lack access to a car, compared to 31% of African American households and 20% of Hispanic households.

Many disparities arise because the market for cars is troublingly opaque and inconsistent. A more consistent and transparent marketplace would not only benefit consumers of color but all marketplace participants, including car dealers, finance entities, and insurers that want to

compete fairly and openly on price and quality on a level playing field.

Recommendations

To move toward this goal, federal and state policymakers should:

Ban dealer interest rate markups. Any compensation paid to the dealer as part of the financing process should not be based on the interest rate or other financing terms, and should be consistently applied to all transactions.

Amend the Equal Credit Opportunity Act (ECOA) regulations (Regulation B) to enable and require the collection and analysis of race and ethnicity data for auto financing transactions.

Prohibit discrimination in the pricing of goods and services.

Increase enforcement of the ECOA and state fair lending laws.

Increase enforcement against general abuses in the sale and financing of cars. Given the evidence of discrimination in the sale and finance of cars, it is likely that many other abuses, from yo-yo sales to failure to pay off existing liens, are more likely to affect people of color. Stepped-up enforcement against all abuses in the sale and finance of cars could help address disparities and level the playing field for everyone.

Take action on insurance rate setting to address disparities based upon race and ethnicity. End suspension of driver’s licenses for reasons beyond dangerous driving.